Via Bill King’s email update. To subscribe, click here.

![]()

The assertion that tax cuts will spur economic growth is now Republican orthodoxy, incessantly repeated by the party’s leaders and surrogates. Most often, these proponents cite the Reagan tax cuts in the 1980s as proof that cutting taxes will boost the economy. But a close look at the historical record shows there is scant correlation between cutting taxes and economic growth.

Immediately after WWII, the highest marginal tax rate on earned income was 91%. Johnson lowered the rate to 70% in the mid-60s. It was unchanged until President Reagan lowered the rate three times, to 50% in 1982, then to 38.5% in 1987 and finally to 28% at the end of his term. The rate stayed at 28% for only three years. In 1991, Bush 41, faced with a growing deficit, raised the rate to 31%. Immediately after Clinton was elected, the top rate was raised to 39.6%. The rate was temporarily cut in the now-famous “Bush tax cuts” to 35%. That cut expired in 2013 and the rate returned to 39.6%.

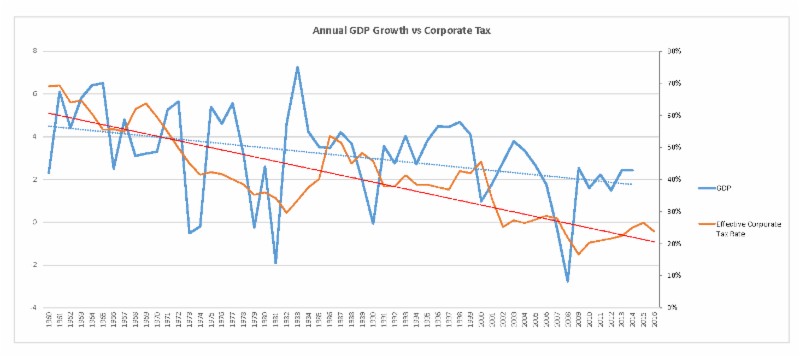

When we graph these changes in the marginal tax rate with GDP growth it is apparent that both have been falling since 1960. If lowering the marginal rates guaranteed higher growth, we should see these moving inversely, i.e., as tax rates came down, GDP growth should have improved. But the opposite is true.

As for the oft-cited Reagan tax cuts, there was a snapback in GDP growth in 1983 and 1984 from the 1982 recession which occurred just after the reduction in the marginal rate from 70% to 50%. But after 1984, GDP growth dropped back to historic norms notwithstanding the additional cuts in 1987 and 1988. By 1991, the country was back in recession.

So, what about cutting the corporate tax rate, which is the centerpiece of the current proposal? Once again, the effective corporate tax rate has also been trending down since 1960. So, neither is there any historical correlation between reducing the corporate rate and economic growth.

So, how are we to interpret the lack of any positive correlation between marginal tax rate cuts and economic growth?

First, of course, we should always keep in mind the fundamental rule of statistics that correlation does not equate to causation, and, conversely, a lack of correlation does not disprove a potential causal link. This is because there are innumerable other economic factors simultaneously at work on outcomes. For example, at the same time the Reagan tax cuts were enacted in 1982, the Federal Reserve was also dramatically reducing interest rates. So, it is very difficult to parse out the effect of changes in tax rates from the other background economic activity.

Second, it may be that the marginal rate and corporate rate are not as important as we think. The Tax Policy Center estimates that the average income tax rate paid by households from 1979-2012 ranged from 17-22%, a much narrower range than the 28%-70% range for the marginal rate during that time.

Also, payroll taxes have been steadily increasing since WWII, both in absolute and relative terms. That rate has more than doubled, from 6% to 15.3%.[i] Payroll taxes as a percentage of federal tax receipts have nearly quadrupled from about 10% in 1950 to just under 40% today.

When you add the payroll taxes and income taxes together, the average tax rate since 1960 narrows even more to a range of 29-31%.[ii] In other words, while the marginal rates have varied widely, the average rate paid by taxpayers has stayed in a pretty narrow range and, as a result, the overall tax burden has changed very little.

Notwithstanding that economists have difficulty quantifying the effects of tax policy on the economy, most nonetheless believe that tax reform, as opposed to just tax cuts, would boost growth. This is because our tax code is both oppressively complex and creates enormous market inefficiencies. The real question is whether the proposals now on the table are the kind of tax reform that will lead to growth or whether it is just tax cuts that may benefit some companies and individuals but have little effect on the larger economy.

Whether the tax reductions will spur growth or not is critical because if the growth fails to materialize, the tax cuts will blow an even bigger hole in the federal deficit. If the tax cuts merely add to the deficit, there may be a short-term sugar high for the economy, but lead to lower growth down the line.

Most economists are skeptical that the proposed tax cuts will even come close to paying for themselves. Twenty-one of twenty-six top economists surveyed by Bloomberg opined that the cuts would increase deficits. Even the President’s alma mater, the Wharton School of Business, has released a study which finds the tax bill will add significantly to the deficit. From what I have read, the consensus among economists seems to be that an increase in growth might pay for about a quarter of the proposed tax cuts. If that is right, the tax cuts will blow a hole in the deficit and lead to lower growth in the future.

The most persuasive analysis I have seen comes from the Committee for a Responsible Federal Budget (“CRFB”). It is co-chaired by Mitch Daniels, the former Indiana Republican Governor and director of the Office of Management and Budget under Bush 43, and Leon Panetta, also a former director of the Office of Management and Budget, White Chief of Staff, and Secretary of Defense under Clinton and Obama. The CRFB disputes that the bill will produce the .4% GDP increase claimed by its backers and projects that the Senate version of the proposed tax bill will add $2.2 trillion to the federal debt over the next ten years. [Click here and here to read.] And that is on top of the deficits we are already expecting, largely driven by the acceleration Social Security, Medicare and Medicaid payments as more Baby Boomers retire.

Regardless of the effect of tax policy on GDP, we should always be attempting to minimize the tax burden on the American people. Every tax dollar collected should be treated as a sacred trust to be spent wisely, efficiently and only for functions for which there is no viable private sector option. But if we pin our hopes for a dramatic economic upturn from just cutting taxes, history suggests we will likely be disappointed and be passing on an even larger federal debt to our children and grandchildren.

________________________________________

[i] This includes the employer and the employee portions.

[ii] The sole exception to this range was 2011-12 when there was a temporary decrease in the payroll tax rate.